-

Call/Text: (425) 379-9200

-

Email: team@autohomeboat.com

5 Common Questions about Classic Car Insurance

Boat Insurance in Washington: What To Know Before You Launch

RV Insurance: What It Covers, Why It Matters, and How to Choose the Right Policy

Stay "On Top" of Your Roof This Spring

10 Tips for Driving Safely in the Snow

Insurance Rates Are Shifting—7 Savvy Things You Can Do to Stay Grounded

7 Proven Fall Tips to Protect Your Home From Wind & Water

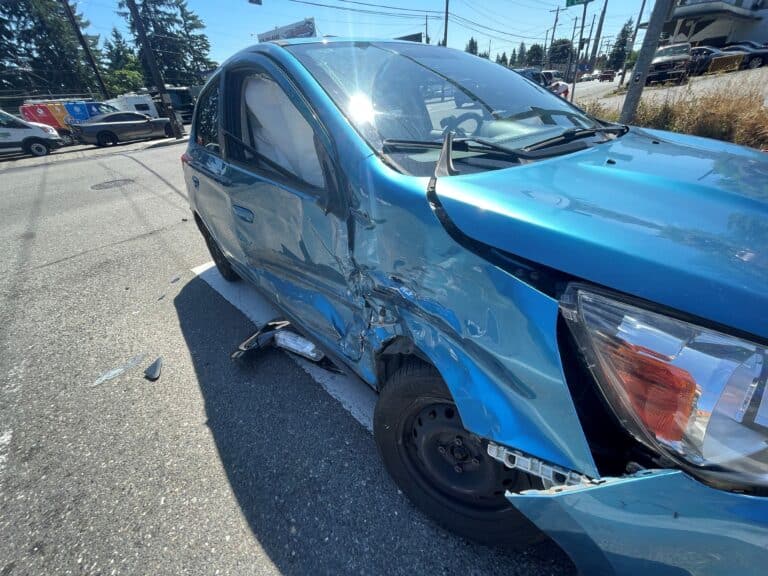

5 Surprising Lessons You Can Learn from Insurance Agents’ Accidents